Humanity feeds percenter thousands of years. We know about enterprising usurers who profit from loans at interest since the VIII century BC. The banking system in the modern sense originated in the XVI century in Italy and is alive to the present time. As for the blockchain, it appeared recently, but has already found numerous applications and adherents around the world. The use of blockchain promises many advantages, but the main is that it allows you to do without intermediaries. Since people can not resist the thirst for profit, it is logical to call for help mathematics and computers. This will reduce the cost of banking services and, for the first time in thousands of years, allow people to trust each other.

Developers are ABLE strive to create the Bank of the future on the basis of the blockchain. The platform will provide financial tools for obtaining decentralized loans. The current financial system is a thing of the past, and existing crypto banks still do not allow you to get a loan directly from the lender. This is because the model copies a centralized system of conventional banks, which deprives users of many advantages of a decentralized system.

The essence of the project

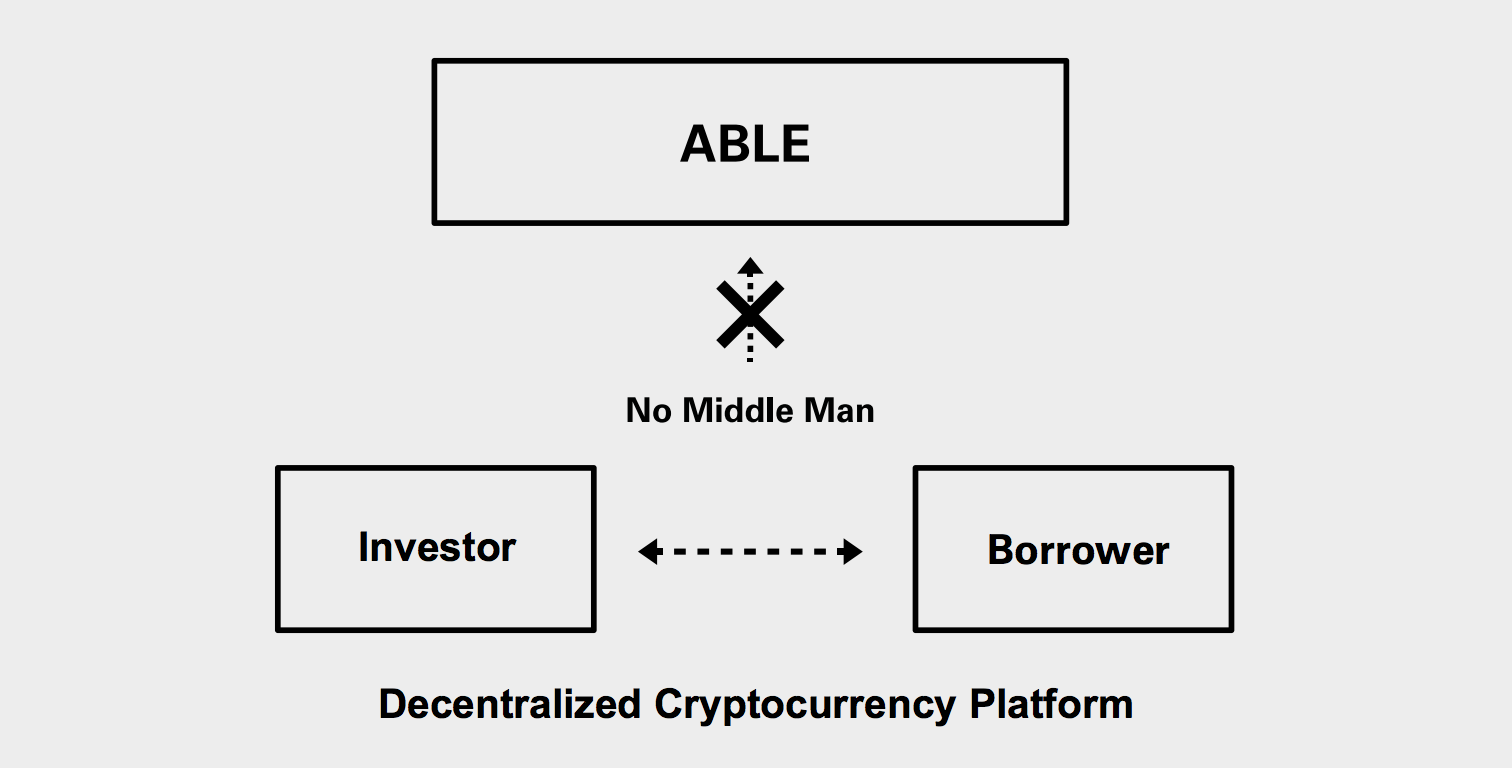

The Bank serves as an intermediate link between lenders and borrowers. Thanks to low Deposit rates and high loan rates, banks make a profit. The idea of ABLE is to remove the intermediate link – the Bank – from the chain. This would allow lenders and borrowers to agree among themselves on the terms of loans.

Thanks to the removal of the intermediary, the profit goes directly into the pocket of the lender. The borrower receives a lower rate on the loan, and the lender gets more favorable conditions than in the Bank. ABLE will use smart contracts to assess the creditworthiness of borrowers.

Traditional banks are centralized institutions that are more vulnerable to hackers than online banks. If the Bank goes bankrupt, both depositors and borrowers will suffer. The use of a decentralized model avoids the risks associated with traditional financial institutions.

In addition, the platform can be used to issue salaries, the developers of ABLE want to replace all the traditional financial instruments that customers may need. All processes are based on the use of smart contracts, which will avoid cheating on the part of other people.

The economy of the token and the details of the ICO

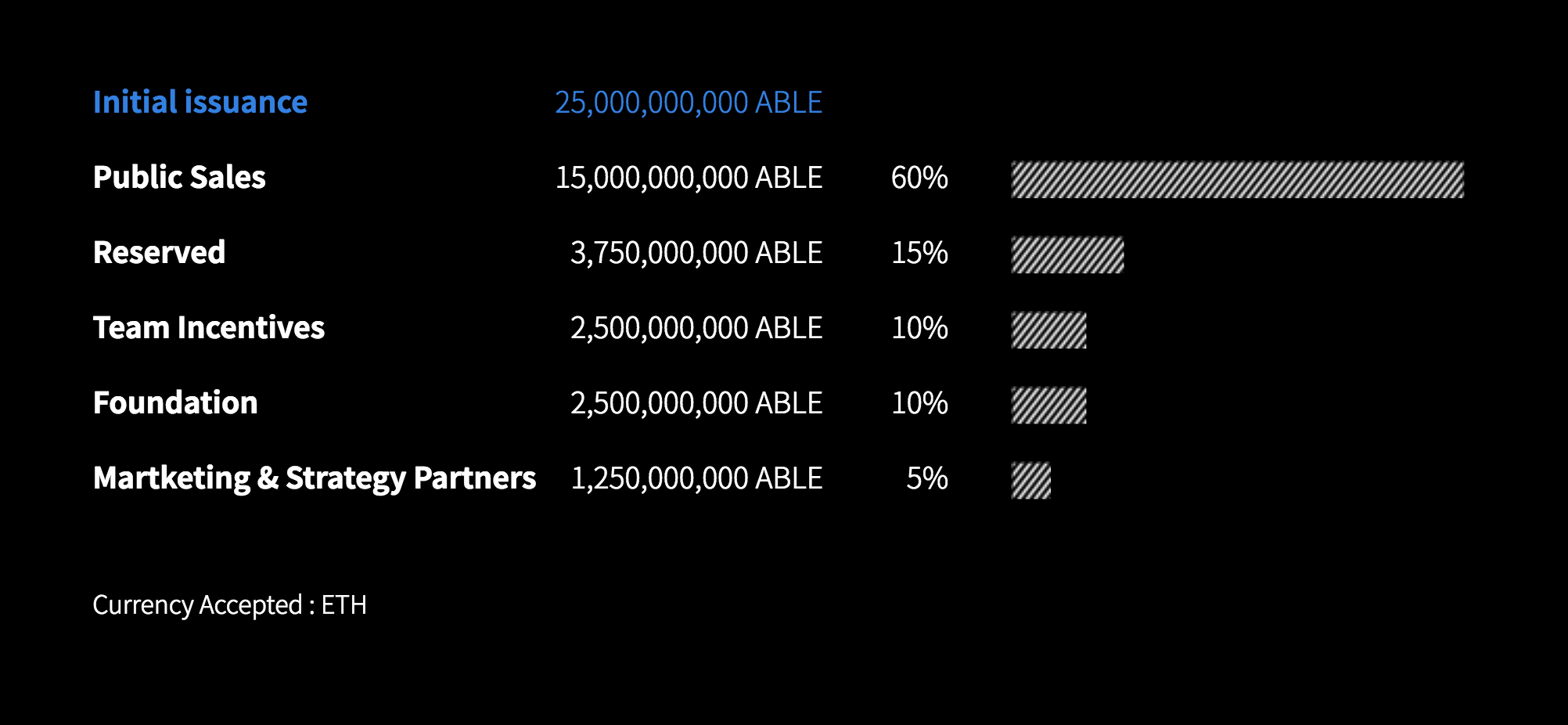

The platform is planned to use two types of tokens, ABLE Coin and ABLE Dollar. With the help of ABLE Coin it will be possible to pay service fees, ABLE Dollar will be used to pay interest. Coins can be exchanged between them. The developers will release 25 billion ABLE Coin and 1 billion ABLE Dollar, the subsequent issue of coins is not planned. The network consensus algorithm is based on proof of stake (PoS), which has a number of advantages for investors.

In total, it is planned to sell 60% of ABLE Coin within the ICO, which is 15 billion coins. Of the remaining coins, 15% will go to the reserve, 10% will be taken away by team members and funders, 5% will be given to marketers and strategic partners. For 1 ETH you can buy 40 000 ABLE Coin.

At the moment has already passed two stages and two pre-sale stage of the sales for the citizens of Korea.

There are two stages of sales on the queue, where tokens will be sold to everyone:

- The first stage will be held from June 27 to July 10, the price of one token is $0.00205. Hardcap – 4 000 ETH, maximum sales-12.7 million tokens.

- The second stage will be held from July 16 to August 10, the price of the token is $ 0.00215. Hardcap is 11,000 ETH, will sell 33.5 million coins.

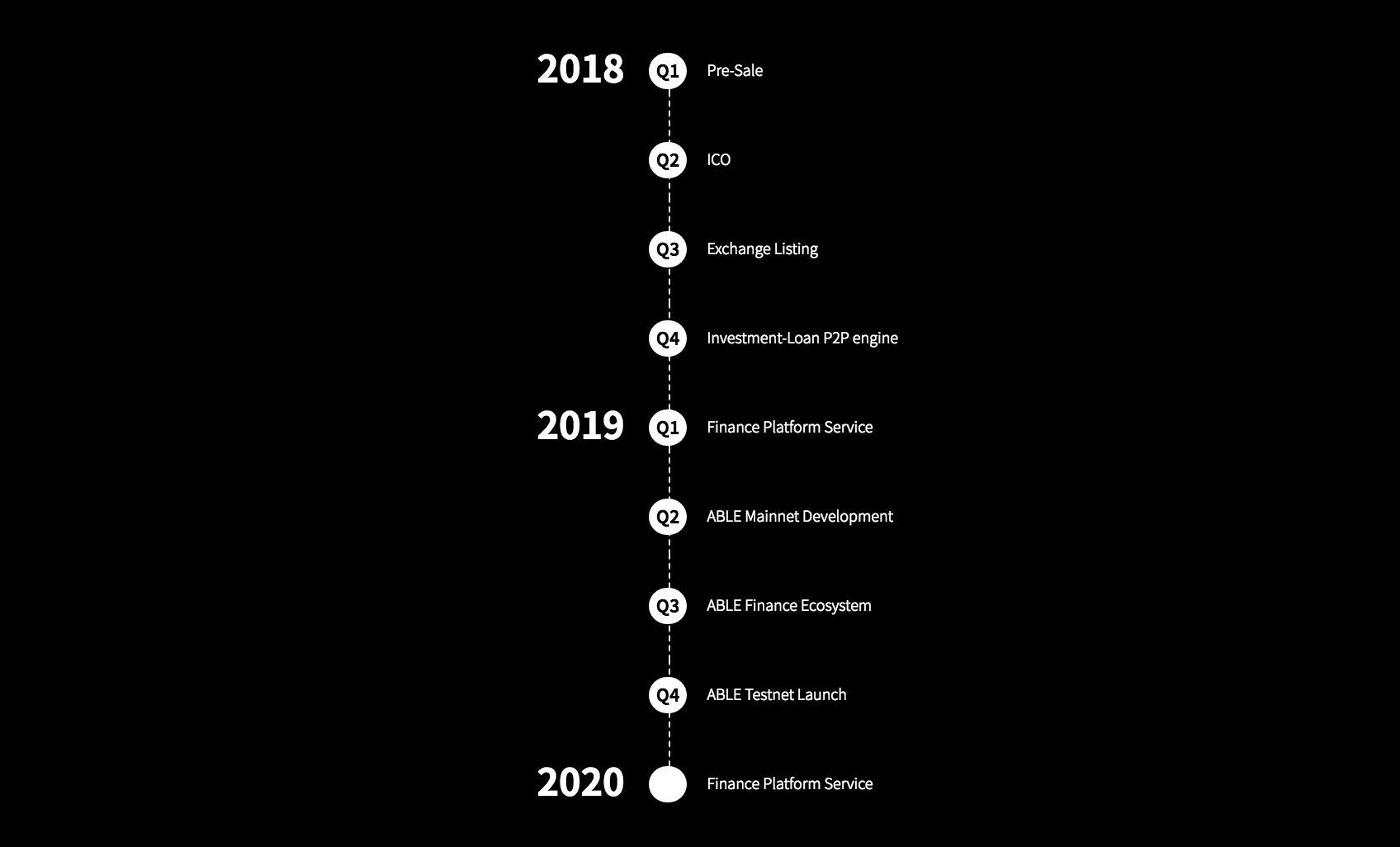

Road map

The project has just started, at the moment there is no finished product or at least part of it. By the end of 2018, P2P services will be developed. The whole 2019 year will be devoted to the development of the main network, financial platform and ecosystem. The test launch is scheduled for the end of 2019, and in 2020 the platform will work in full force.

Conclusion

The task of the project is to solve urgent problems in the field of Finance. Please note that most of the development team - are citizens of Korea, and presale was held exclusively for the inhabitants of this country. Perhaps this suggests that ABLE is rather focused on the Asian market, at least the desire to keep most of the platform's capital in one country is evident. Thanks to the use of PoS, we can already say that the consensus in the network will be mainly Korean. The idea of centralizing the shareholders of a decentralized project is quite strange and unusual.

In the world market of decentralized loans, developers will face intense and serious competition. The reality is that those who want to implement a revolution in the world of Finance and to be at the head of the inevitable process of change – more than enough.

Since the finished product has not yet been presented to the public, it is too early to judge its prospects. What the team does not hold, so it is thoroughness-in the text of White paper you can find a lot of details about ABLE and there is no information about the planned distribution of funds. The documentation is likely to be finalized and become more detailed in the near future.

Official resources of the project ABLE:

TELEGRAM: https://t.me/ABLE_Project_EN

TELEGRAM: https://t.me/ABLE_Project_EN

Username : Ozie94

eth : 0xDa2F65ea0ED1948576694e44b54637ebeCA22576

No comments:

Post a Comment